Employee compensation represents one of an organization’s biggest and most crucial investments. With the right compensation structure in place, an organization can hire and retain great talent to drive profitable business. On the other hand, a poor compensation structure can lead to a talent crisis or trouble maintaining profitability.

Unlike so many other elements of business or HR, executive compensation is not simply a matter of best practices. While industry benchmarks are an important part of the formula, any compensation strategy should focus on the unique needs, goals, strengths, and culture of the organization.

Looking forward, we’ll explore some of the main ideas from the webinar, including:

• The value of planning and alignment when it comes to executive compensation

• Creating alignment with a business’ cultural and philosophical values in mind

• Leveraging equity effectively as part of a compensation strategy

• Creating a bonus structure that’s scaled to your business

The Power of Planning and Alignment Executive compensation would probably be a lot easier if all businesses were the same, but the incredible variety of industries, business types, and corporate cultures in the marketplace means that one-size most certainly does not fit all.

In order to succeed in such a wide-open game, organizations must articulate a clear, well-thought-out strategy to guide their approach to talent acquisition and retention that’s built on a deep understanding of what their business is, where they are today, where they’d like to go, and what they need to do to get there. By focusing on compensation strategy conceptually and not just hiring and compensating employees one-off, businesses can create a more cohesive culture that’s aligned with business goals.

For example, in the case of startups, many key players (especially executives) are often brought onto a team one at a time. This creates a flexible situation in which many early-stage companies create a variety of different salary points, equity offers, and bonus packages on an ad hoc basis to fit employees as they hire.

While that model works well for some startups and may be tempting in the short term, it can be disastrous as a basis for a long-term compensation structure for several reasons. First of all, planning compensation one employee at a time makes it easy to lose the forest for the trees. That means that, after several years of hiring, employees throughout the company could command salaries and benefits packages that have little to do with their current value to the organization and better reflect how desperate the company was for talent at the time of hire.

Additionally, working on a case-by-case basis without a well-structured, well-aligned plan in place can wind up producing a pay scale that feels unfair and demotivating for workers just a year or two in. The more transparency and logical explanation an organization can provide about how compensation works, the more likely they are to connect with discerning talent.

When a business builds a consistent, richly-planned, well-articulated compensation structure, it tells the workforce, “Everybody here is valuable, and we are in this together.” By planning a consistent approach to compensation from the outset, organizations can create a well-scaled core team with a healthy culture that’s positioned to drive both innovation and profit.

Planning with Values and Goals in Mind If self-knowledge is the key to compensation alignment, the next logical question is, “What kind of self-knowledge do we need?” The short answer to that question is “as much as possible,” but let’s take a moment to think about some specific questions businesses’ should ask themselves about their organizational values and goals as they build a compensation strategy.

Revenue vs. Profit vs. Innovation – The way leaders are compensated must directly reflect their ability to drive business success. With that said, there a variety of different ways to quantify that success depending on a business’ size, position in the marketplace, and growth targets.

A strong approach to executive compensation must identify key growth indicators or KPIs and ensure individual success is aligned with company success. That means compensation strategies may shift as the organization evolves, but only in mindful ways that reflect the work at hand and upcoming goals.

Individual vs. Team Performance – Some businesses are about achieving results no matter what and elevating the difference-makers who got there when others couldn’t; other organizations emphasize collective or team-based success. Each scenario requires a specific approach to compensation, and a lack of philosophical alignment only sets everybody up to fail.

Make no mistake, incentivizing individual achievement or teamwork will directly and strongly shape workplace culture, which reinforces the importance of planning with organizational goals and values in mind before designing compensation packages out of thin air. Both models can be successful in different scenarios, but once again, it’s a matter of industry, goals, and organizational self-knowledge.

Short- vs. Long-term Performance – It wouldn’t be fair to judge or compete in a race if the distance wasn’t established ahead of time. By the same token, the effectiveness of leaders can’t be fairly judged without a business articulating what they really value and expect.

Some organizations philosophically prefer a slow and steady pace; others are innovation-minded and would rather someone step up to the plate and hit a home run than maintain a solid batting average for several years. Again, both styles can work, but getting caught between the two in terms of articulation or finding compensation out of alignment with organizational goals can both be costly.

Aligning Different Elements of Your Compensation Package Any compensation package includes a salary, employee benefits, and often for executives, equity and bonus opportunities. For a compensation structure to truly work, all those pieces of the pie must be balanced in a way that works for assets and the company alike, building reward, incentive, and buy-in.

Let’s think about how different elements of that compensation puzzle can be implemented or leveraged depending on company goals, size, and industry.

Balancing Base Salary – Base salary is probably the least “unique” piece of a compensation package, as it is generally strongly informed by industry benchmarks. With that said, salary can be adjusted on a sliding scale based on organizational values and growth goals.

For example, an early-stage organization prioritizing growth, innovation, and short-term performance can create strong bonus incentives for executives (more on that later), allowing the organization to place less emphasis on salary. On the other hand, larger, more established businesses who are years or decades past their IPO can align their compensation structure to their market positioning by putting greater emphasis on salaries.

Intelligently Leveraging Equity – In almost any for-profit business scenario, the business itself is the owners’ primary asset. When experienced executives see a profitable idea or great business model, they want to get in on the ground floor and grow along with that company. That means equity offers can be powerful incentives for executives and other leaders to drive growth, achieve milestones, and stay bought in for a half-decade or more.

On the other hand, some organizations’ goals or financial positions might make it advantageous to protect equity. That can be a successful and profitable long-term strategy as well, but in order to win with great talent, those organizations will need to pump up other aspects of compensation, such as salary or achievable bonuses.

Again, the key either way is to articulate a consistent approach that’s aligned to company goals and drives growth – not just to land talent by offering them stock options.

Building an Impactful Bonus Structure – Startup culture has made equity compensation so attractive over the last 20 years that cash bonuses are often forgotten as part of a winning compensation strategy. With that said, a well-scaled bonus structure is a fantastic tool for keeping leadership engaged and maximizing each project or initiative.

Bonuses invite employees to succeed and celebrate alongside the organization they work for and see the true connection between their great work and company growth. In this way, bonuses reward assets for their direct, impactful alignment with company values and goals. That’s why bonuses are great buy-in tools and motivators, both in the long- and short-term.

One of the best ways organizations (even small or medium-sized ones) can provide impactful bonuses that show clear alignment with company values and goals is to provide ad hoc rewards. Essentially, ad hoc bonuses are cash rewards distributed to leaders and/or team members when specific goals are achieved. An ad hoc bonus could come at the end of a timely development sprint, at the completion of a key project, at the closing of a major account, or any other time for organizational celebration.

Conclusion/Takeaways Creating a winning executive compensation structure is highly complex because no two businesses are alike. Remember: • Executive compensation must be aligned with organizational goals and values in order to succeed • Salary, equity offers, and bonuses can all be structured, balanced, and leveraged in different ways depending on company size and objectives, but the compensation structure must match be built purposefully and account for the uniqueness of the organization

Amid legislation that pushes consumerism in healthcare while putting greater burdens on healthcare consumers, employers and employees alike have turned to high-deductible health plans (HDHPs) to minimize their healthcare costs. As premiums continue to rise, these plans offer an opportunity to keep upfront costs low for companies and their employees. At the same time, the IRS permits the creation of tax-exempt health savings accounts or HSAs for people with HDHPs to cover the costs of the higher deductibles when expenses do come up.

This system works great for everyone involved – so long as people stay healthy. Which makes preventive care an integral part of any successful HDHP based healthcare strategy. By allowing patients to head off health issues before they become significant expenses, preventive care keeps everyone’s expenses down and maximizes health outcomes for the insured. Recognizing this, the IRS has allowed insurance plans to cover preventive care such as check-ups, screenings, immunizations, and tobacco cessation or weight-loss programs with a low or non-existent deductible while keeping their HDHP status.

However, the IRS has not generally extended the same low-deductible permissions to treatments for existing illnesses or conditions. Since 2004, certain on-the-spot treatments for conditions discovered during screenings (such as removing polyps discovered during colonoscopies) and medications to prevent recurrence of heart attacks or to reduce cholesterol to prevent heart disease have fallen under the umbrella of preventive care, but that’s about it.

Which means that people with chronic conditions have generally been left out. They have had to choose between paying out high-deductibles for treatments that prevent their conditions from worsening, or giving up their HSAs and adopting high-premium plans. Until now, that is.

The IRS’ New Rule

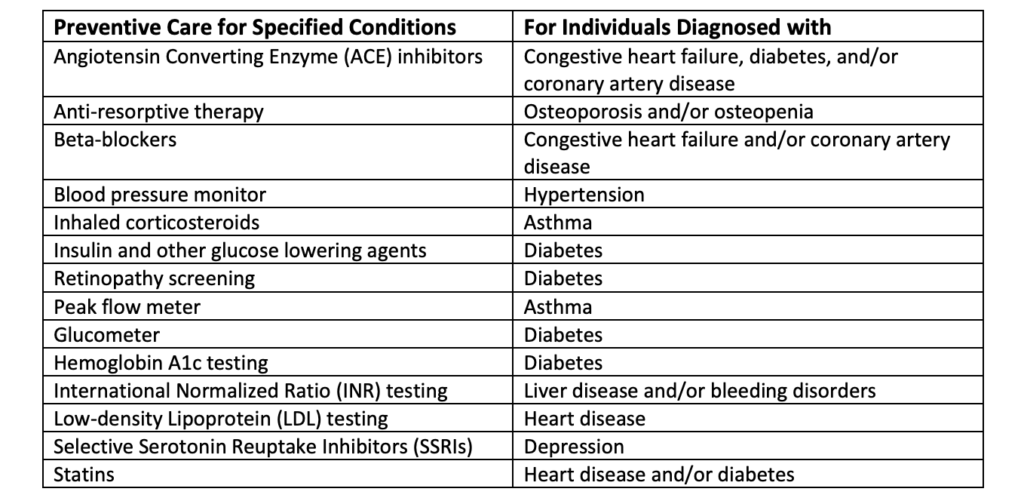

On July 17, 2019, the IRS issued Notice 2019-45, which significantly broadened the definition of preventive care to extend it to many treatments for chronic conditions. To qualify as preventive care, the treatments must be likely to prevent the worsening of a chronic condition or the development of a secondary condition which would incur greater healthcare costs. It must also meet several other criteria, which we have outlined in this handy chart for easy reference:

The Impact for Companies and Their Employees

So what does this policy change mean for employers and employees? Simply put, it provides enormous opportunities for both to take greater control over their costs, minimizing their expenses while maximizing employee health and wellness. It makes the already appealing HDHP and HSA healthcare option a win for employees who want to increase their welfare and for employers who are looking to reduce their expenses.

The expanded definition of preventive care provides a new opportunity for employers to educate their employees so that they can become more intelligent consumers amid government policies which force consumerism in the healthcare market. Employees can use HDHPs to control their costs without fear of compromising their health, especially by neglecting chronic conditions to avoid paying high deductibles. Instead, they can get the treatment that they need at low costs while keeping their tax-exempt health savings.

Key Takeaways

We’ve thrown a lot of information your way in this article, so here are some key takeaways that you should remember:

• IRS Notice 2019-45 opened up serious opportunities for employers to cut their costs and for employees to reduce their expenses and maximize their healthcare outcomes

• Chronic conditions will no longer force consumers to take on significant healthcare costs to receive the treatment they need to maintain their health and avoid future expenses

• That means that high-deductible health plans, which already provided the best solution for consumers in the current healthcare market, are now better than ever

To make the most of the rule change as an employer, you should partner with a proactive benefits broker who will help you craft a healthcare strategy which maximizes the impact for your employees while minimizing your costs. Benefits are an important tool to attract, retain, and engage the talent that you need to grow your business. The well-being of your company and its employees ultimately depends on the effectiveness of your benefits strategy. So it is more important than ever to work with the right benefits broker.

Interested in making the switch to a broker who is invested in your growth and your employees’ well-being? Start the conversation today.

When was the last time you considered how well your employee benefits broker was performing? In the intense war for talent that we’re now experiencing across industries, you can’t risk overlooking any aspect of recruitment and retention strategy.

Employee benefits are one of your most effective tools to attract top talent and retain the top performers you have. With more open jobs that unemployed people currently in the US, recruiters and executives must do everything possible to keep their organization competitive in the talent marketplace.

The employee benefits broker your business works with plays a large role in how impactful your overall benefits offering in your ability to attract and retain talent. Think through the crucial questions outlined in this post will help you ensure that you’re working with a benefits broker that’s doing the most for your business.

1.Conduct a straightforward costs and benefits analysis

First of all, the amount of money you put into your employee benefits program is no small expense for your company. For most companies, benefits are the second most costly expense, just behind salaries, according to data from the Society for Human Resource Management (SHRM). So, it’s a smart decision to enlist a skilled benefits broker to ensure those costs are kept low while driving the maximum value for your business. But you must consider how much value is your current broker providing to your business? And what are the measurable advantages that you can directly correlate back to their services?

The truth is, your broker may be providing subpar services that aren’t getting you the results you want or need (or that are visible to employees). What you need to happen: the money you put into a benefits program is well spent, and you don’t have to continuously worry about what your funds are going toward. You have too much on your plate to have to then keep tabs on your benefits broker, so review your current benefits program and employee satisfaction level to determine if your broker is meeting the mark.

2. Consider the latest technologies: Is your broker keeping up?

Approaches to employee benefits administration continue to be updated based on what’s happening in technology and business intelligence. When was the last time you had a conversation with your benefits broker about how they’re using these advances to push forward your company’s benefits strategy? If this conversation has never been had, or if you feel like your benefits broker isn’t using some of these technologies the way they could, it may be time to find a new employee benefits consultant.

Part of your role in choosing a benefits broker is ensuring that you find someone who not only recognizes the importance of proactive change, but who also incorporates these updates into the way they do business. It should be their responsibility to know what’s hot in the benefits market and what high-quality candidates are looking for, so that they can make effective recommendations to you and your team about offerings and updates. If your employee benefits broker is behind the times, your benefits package will be, too. And if that’s the case, you’ll have a much more difficult time attracting and retaining the best talent.

3. Assess business growth (or lack thereof)

If your organization is growing, chances are you need to make updates to many of the vendors or consultants you work with. Benefits brokers are no exception, as these professionals typically have specialties in regards to the size, industry, and culture of the companies they work with. If your workforce is growing rapidly, it may be time to assess whether a different broker would bring you better results.

When your company changes, it’s always a good idea to take a look at if your benefits broker can still provide the level of services you need. It may be especially smart to look at current and historical growth information and projections around the time when it’s time to think about revamping your employee benefits package for the coming year.

4. You haven’t looked around in a while

It’s of course easy to let consultant-shopping fall by the wayside once you’ve hired someone and have gotten used to working together. But when was the last time you looked around to see what else is out there? Even if you don’t end up hiring a new benefits broker, just taking this step could mean that you will reaffirm your decision in hiring your current broker. You may already have the best, most cost-effective person for the job—but you’ll never know if you don’t keep up with your research. If it’s been more than three years, as the SHRM suggests, start shopping for a new broker now, even if you don’t take any further steps forward beyond exploring your options.

5. Service and communication have been lacking

We’ve all experienced when a vendor just isn’t performing up to par. It can be easy to make excuses for these professionals or to hand out too many second chances, especially if we like the person and really want the business relationship to work out. But, we often end up having to do more work than we should be doing in these instances.

Remember: you’ve hired a benefits broker for a specific job. Really think about if they are providing every required aspect of that job, and ideally going above and beyond what is expected to provide the highest level of service. If you’re having to correct their mistakes, call or email them more than once for a response, or remind them about deadlines or new strategies to try, it’s probably time to call it quits and find a broker who will step up and provide everything you need.

6. Employees aren’t satisfied with the benefits program or with the enrollment process

In today’s candidate-driven job market, employees are often on the lookout for a better position. Even if they’re satisfied with their work, their role, and their company, they are always keeping their eyes open to make sure there isn’t something even better out there. One survey conducted showed that 78% of people are open to new jobs in 2019, and 38% reported to be actively searching for a new role.

Benefits play a large role in employees’ decisions about whether to stay or leave. So how happy are your workers with their current benefits package? You may hear complaints or praise at lunch or in the hall, and that could be helpful information when you’re starting to think about your benefits broker. Or, you may even want to implement a benefits survey where employees will feel encouraged to share what they don’t like or what they’d like added in the near future.

This can be a great way to find out if your benefits broker is getting you the package that includes everything the modern employee wants, from plenty of parental leave to gym memberships to excellent health and dental packages, and more.

But, there’s more to benefits satisfaction than just the benefits themselves—employees also care about the benefits portal and having easy access to benefits information. Assess whether information is readily and easily available to all employees.

What kind of benefits technology does your current broker use? The enrollment process should also be streamlined and simple so that employees aren’t dealing with a big headache once a year to get the benefits they want and need. You need a broker consultant who will use the latest tools to ensure that processes are simple and transparent for your employees.

Key takeaways

The person behind your employee benefits package and process has a lot of influence on employee satisfaction and your ability to attract high-quality candidates. When you’re assessing whether it’s time to find a new benefits broker, consider:

If the costs versus benefits are aligned

If your broker is keeping up with the latest trends and technologies

If your organization has grown significantly and may have new needs that your current broker can’t provide

If it’s been more than three years since you shopped around

If your broker’s communication and services haven’t been up to par

If employees are complaining or aren’t satisfied with their current benefits package

If some of these considerations are true for you and your organization, it may be time to start shopping around for a new employee benefits broker. Remember that before you make a selection, it’s important to list all the ways your previous broker was not meeting expectations so that you don’t make the same mistakes again.

A Williams Institute study in 2018 found that 4.5% of the U.S. population self-reported identifying as LGBT (Lesbian, Gay, Bisexual, or Transgender). The real number is probably much higher, as diversity and inclusion expert Stephanie Huckel’s work suggests as many as 46% of LGBTQ professionals feel compelled to hide who they truly are in the workplace, which means any formal study probably skews quite low in terms of representation.

Any successful HR professional or C-suite executive knows that no team member, no matter how intelligent, focused, and driven can truly do their best work in an environment where they don’t feel safe to be themselves. Maximizing productivity and buy-in from LGBTQ employees and their allies requires creating an environment where people are valued and protected in a way that’s both inclusive and transcendent of their sexuality or gender identity.

Moving forward, we’ll explore:

• The unique legal position of LGBTQ professionals

• Why LGBTQ-inclusive policies build a stronger, better organization

• Some general guidance for creating LGBTQ-inclusive practices

Addressing the Additional Stress on LGBTQ Professionals

Gay, lesbian, bisexual, and transgender professionals have disproportionately felt the pain of discrimination in hiring, firing, and promotion scenarios and continue to deal with explicit or exclusionary workplace harassment, even as it has universally unacceptable to target other protected groups in similar ways.

Some HR leaders and organizations find it hard to understand why their policies and procedures need to contain explicit language about LGBTQ non-discrimination or contain specific guidance about potential issues like homophobic harassment or gender transition procedures. The unfortunate current state of affairs is that LGBTQ professionals receive only patchy, implied federal protections, which means that unless their employers take a strong, proactive, supportive stance, their employment status can feel extremely vulnerable.

Title VII of the Civil Rights Act protects individuals from gender or sex discrimination, but only conventional interpretation extends those protections beyond the definitions of “sex” and “gender” that were understood in 1964, when the law was written. While there have been efforts to expand the language of Title VII to create explicit protections for LGBTQ individuals, that work is currently stalled.

Those prevailing interpretations mean that LGBTQ professionals can file harassment or discrimination claims with the EEOC (Equal Employment Opportunities Commission), but that is a long, expensive process that often draws out the agony of harassment and can potentially negatively impact the victim’s future career prospects.

That inconsistent or just-implied federal support leaves an incredible spectrum of different professionals feeling like they have less agency and recourse in the workplace than their non-LGBTQ peers. With that said, almost half the states in the country have created laws that protect against gender identity and sexual orientation discrimination for both public and private workers.

• Western States with LGBTQ Workplace Discrimination Protections: Washington, Oregon, California, Nevada, Utah, Colorado, New Mexico

• Midwestern States with LGBTQ Workplace Discrimination Protections: Minnesota, Iowa, Illinois

• Eastern States with LGBTQ Workplace Discrimination Protections: Maine, New Hampshire, Vermont, Massachusetts, New York, Rhode Island, Connecticut, New Jersey, Maryland, Delaware, and Washington, D.C.

Businesses operating within any of those states are held to a reasonably high standard for LGBTQ inclusion, with a framework in place for wronged individuals to gain the protection of the court system and punish businesses for discriminatory practices or creating a culture of normalized harassment.

With that said, even in those states, the existence of a legal framework for recourse does not mean the non-existence of harassment or discrimination. Preventing those initial hurtful episodes still falls to each individual employer or workplace, and the businesses who master creating a fully-inclusive workplace will win over the trust and gain the ability to leverage the incredible skills of the LGBTQ workforce.

On the other hand, for LGBTQ citizens of the other 29 states, there is incredible need for either public or private protections. Some counties or cities have passed local non-discrimination laws to provide protections for their LGBTQ workforce and residents, but that means job hunting for many involves using a map of potential landing places that looks like Swiss cheese.

In areas where no public protections exist, LGBTQ professionals must rely on their employers to create, maintain, and enforce their own policies and procedures to prevent harassment and eliminate discrimination. Given both the historic struggles of the LGBTQ community and the historic struggles between employers and workers, it’s easy to see why many feel extremely cynical or insecure in that position.

With that said, businesses in those areas with no public protections who forge meaningful, inclusive policies that invite LGBTQ workers to be themselves, feel comfortable in their work space, and get powerful back-up from their employer have the opportunity to get first pick at an incredible pool of business-driving talent.

From an organizational perspective, LGBTQ inclusion is much bigger than the basic decency of protecting employees from discrimination and harassment. It’s about creating an environment where assessments of someone’s proficiency, abilities, and strengths or weaknesses are made based on performance data and demonstrated results, not assumptions. It’s about fostering a community where everybody’s insights, perspectives, and strengths are leveraged to the maximum through positive interdependence, shared goals, and empathy.

When businesses do that right, they set themselves up to win big in a few different ways. Let’s pause to explore how LGBTQ-inclusion is a matter of best practice.

It’s the Right Thing to Do Profit has historically been valued above “doing the right thing” for businesses, especially large ones, but that’s starting to change culturally. In the current atmosphere, it’s more important than ever to consumers (and therefore the bottom line) that businesses operate in an inclusive manner.

Directly aligning a business or brand with strong, progressive values is no longer seen as a boat-shaking move that could scare off customers; on the contrary, numerous large businesses have seen themselves called out by consumers and advocacy groups in recent years for failing to articulate inclusive policies.

By being proactive about LGBTQ inclusion, a business shows their employees, prospective employees, investors, competitors, consumers, and the market in general that they’re concerned with talent, not exclusion.

Building Authentic Buy-In from Workers Given the high percentage of LGBTQ workers who do not feel comfortable sharing their status in the workplace and the number of employees who do not report incidents in which they’re made to feel uncomfortable, it’s impossible to truly quantify how much productivity, innovation, and morale are lost each year due to inclusion gaps. With that said, any number is too high.

By creating a strong, supportive environment where inclusion feels like a true value and not just a legal concern, organizations can invite workers to feel both more invested and safer in a way that leads to better work and a healthier environment. When employers feel like allies and not just bosses, there’s more incentive to invest in the work and succeed together.

Equipping Leadership with the Tools to Solve Problems When businesses aren’t proactive about policy, they often find themselves dealing with problems they don’t really have the tools to solve. On the other hand, proactive planning means that when a negative scenario (such as a problematic employee) does present itself, there is a procedure in place by which the problem can be handled and removed in a way that is richly-documented and will hold up in court.

Staying Ahead of Regulation Depending on the outcomes of upcoming elections, significant increases in federal and local protections for LGBTQ professionals could be on the horizon. Businesses that have already articulated internal policies and created a strong, inclusive environment will be able to transition smoothly into whatever new framework might be created, while organizations that lagged behind get into dragged into accountability and regulation leave themselves vulnerable to potentially costly and reputation-damaging disasters.

In the world of business, it’s always important to be perceived as an innovator on the cutting edge. In the new talent marketplace and culture, being a human rights innovator is just as important as being a financial innovator. Inclusion is just one more way that a business can be ahead of the game in the quest to connect with talent and maximize organizational reputation.

Guidelines for Creating an LGBTQ-Inclusive Environment

Building a company that wins through inclusion requires long-term commitment, vision, and strategy, but here are a few tips to help guide organizations looking to articulate LGBTQ inclusion policies and procedures:

Policy creation • Nomenclature: It’s important everybody in the workplace uses appropriate, professional terminology. Company policies should spell out acceptable and unacceptable terms and establish clear guidelines for workplace conversations. Furthermore, guidelines for appropriate pronoun use should be created and enforced for transgender and non-binary workers. • Clearly articulated harassment/discrimination guidelines: As we said before, in order to create a strong, inclusive environment, businesses need to give themselves the tools to enforce the culture of inclusion and weed out bad apples in a richly documented, legally appropriate way. -Reporting process – It’s not enough to say, “discrimination and harassment are bad;” it’s essential to have a well-organized, transparent, and trustworthy system that employees know how to use to report issues. -Staffing for support – Policies need to be backed up by human faces who are dedicated to inclusion, equality, and building the best possible workplace culture. Working with a trusted HR partner such as Launchways can connect your team with actionable equality policies while mitigating the need for your business to hire an in-house support person. • Ensuring there are no employee benefits gaps for LGBTQ professionals -Comprehensive healthcare coverage that connects transgender, non-binary, or intersex professionals with the doctors they need is essential to keep the workforce healthy and provide equality. -Transition support programs for transgender individuals must be available. -Life insurance and other policies that account for non-binary identities and non-heteronormative concepts of family must be available.

Employee Training • New Employee Orientation must introduce LGBTQ inclusion policies and hold hires accountable for knowing them. • Allow for an evolving world by having a dedicated HR professional stay up to date on emerging themes and issues of LGBTQ inclusion and providing on-going professional development or training as needs are identified. • Authenticity is required for employee education to really work. Meaningful role play and powerful, relevant speakers are required to make laggards take these issues seriously. • Documentation of training creates a strong framework for accountability.

Fostering an Inclusive Culture • Show organizational dedication to LGBTQ inclusion by adopting a relevant cause, raising money for a relevant charity, or raising awareness of LGBTQ issues in your local community. • Create a welcoming, positive environment where people are treated as human beings with dignity and valuable assets with potential and skills. • Make HR a driving force in pushing both leadership and rank-and-file workers to make inclusion, diversity, and LGBTQ rights key values.

Conclusion:

LGBTQ inclusion is one of the most important issues facing businesses in the current climate. In order to connect with and retain great talent, organizations must demonstrate their commitment to fully supporting each individual worker in their professional journey, regardless of their sexual orientation or gender identity. With potentially increased regulation looming, the businesses that are proactive will be the ones who articulate the best policies and align their corporate cultures with the winds of change.

Key Takeaways:

• LGBTQ professionals current receive patchy federal and state protection from workplace discrimination -This can make the workplace a place of increased stress and anxiety, which means workers can’t be their best selves • Regardless of local laws, businesses who proactively adopt LGBTQ-inclusive policies set themselves up to win with talent and build a future-facing organization • Policies must be articulated clearly and explicitly designed with the needs, challenges, and support of LGBTQ professionals in mind in order to truly make a difference

One of the main reasons why many companies stay with the same benefits broker year after year is because they have a personal relationship with them. Maybe they’re brothers-in-law, golf buddies, or business school friends. There’s a good reason for that – connections are important for business success, they might feel more comfortable being upfront with a broker they know, and sticking with the same broker can give a sense of stability often lacking in a growing business. But at the same time, these relationships often cause businesses to stay with the same broker even after they have stopped providing the highest level of service.

No matter how great, personal, and long-lasting your connection is with your current broker, it is always a good idea to reevaluate the relationship. This does not mean just ditching your current broker because there might be someone else out there who will do more for your business. It simply means taking an honest look at your current broker to see if they are still doing everything possible to help your company grow and succeed. And then, if you have doubts, looking at what competitors are offering to see if you could benefit your business by switching brokers.

If that idea makes you uneasy, we get it. Honestly evaluating your business relationships and potentially changing them can be difficult and sometimes painful. It’s much easier to just let things stay the way they are. But if you do, you will be doing yourself, your business, and most importantly, your employees, a huge disservice. So we’ve broken down the steps that you can take to make sure that your current broker is still the best fit for your business, no matter what relationship you have with them. In this article we’ll explore:

• Why You Should Care About Your Broker

• Risks and Rewards of Working with the Same Broker

• How to Evaluate Your Broker

• What to Do When Your Broker is Friends with Your CEO

Why You Should Care About Your Broker

Many growth-stage businesses treat benefits as a necessary evil and as such, they choose the path of least resistance. This may mean working with their buddy, or it could mean working with a broker who doesn’t push them think about their long-term benefits strategy, even if that means that their employees end up with subpar benefits at a higher cost. But the fact of the matter is that employee benefits are a crucial component to the success or failure of a growing business.

Benefits spend is generally the single largest talent-related cost after base salary. That means that minimizing benefits expenses is extremely important to the financial sustainability of growing businesses, especially given the small margins most operate upon. You want to work with a broker who does absolutely everything that they can to reduce your benefits spend while maintaining or increasing the quality of benefits for employees.

And benefits don’t just matter to your bottom line. They are one of the biggest tools in your arsenal to attract, retain, and motivate top talent. According to Aflac surveys, most employees would accept a job with lower compensation but a better benefits package. And the same survey found that 80% of employees believe that their benefits package influences their engagement in their jobs. Building an effective, motivated team of talented employees is vital to the success of any business. But many struggle to compete for talent against large companies with greater resources. A targeted, intelligent benefits strategy which maximizes impact while minimizing costs can help growing businesses attract the talent that they need.

To have this impact on your employees and your finances, though, you need to work with a benefits broker who understands your unique needs and who is constantly working to update and optimize your benefits package. It’s not enough to set up your benefits package and then forget about it or to work with the same broker year after year without considering whether they’re delivering the maximum value for your business (even if they are your brother-in-law).

Risks and Rewards of Working with the Same Broker

Are there plus sides of working with the same broker, especially if you have a close relationship with them? Of course there are. They might advocate harder for your business because of their relationship with you, provide more personalized service, and serve as a more effective sounding board for your benefits strategies. Plus, it’s nice to do business with someone who you know and like.

At the same time, though, those same feelings that give you pause about the idea of changing brokers can also hold you back from being a fierce advocate for your business and its employees. You might be afraid of damaging your relationship by pushing your broker to provide the most effective, and affordable, benefits package possible. Failing to keep business relationships and personal relationships separate can often lead to sub-optimal business results or even conflict and damage to both relationships.

And it’s not just your attitude that matters. Most brokers, no matter how good their intentions are, will start taking accounts that they feel are ‘safe’ for granted. They’ll focus their time and resources on pleasing their new clients and acquiring new accounts. And no account is safer than one that is secured by friendship or family connection. Your brother-in-law or college buddy might well work extra hard to get you a good deal when setting up your benefits package. But chances are that they’ll start taking your business for granted, especially as the years pass by. The level of service will decrease, your benefits package will get outdated, and you will lose your competitive edge to attract and retain the talent you need to succeed.

How to Evaluate Your Broker

There’s no harm in finding out whether or not your current broker is providing the maximum value to your business. Taking an honest look at your benefits strategy and your benefits broker only helps you improve your employees’ lives and your business’ finances no matter what you decide to do with the information.

So how do you tell whether your broker is still the best fit for your business? Here are some key things to ask yourself when evaluating your broker:

• Have they updated your benefits package recently? If your benefits haven’t changed in a long time, it’s likely your current broker isn’t taking a critical look at how to constantly improve your offering.

• Are they working with you to refine your benefits strategy based on your business needs and the needs of your employees?

• Can you demonstrate ROI to justify your investment in your broker?

• Is your broker working with you to develop innovative solutions to maximize value and minimize costs?

• Does your broker identify and address your employees’ real needs? Brokers can conduct employee surveys and health-risk assessments (HRAs) to identify employee needs and adapt your benefits strategy to meet them.

• Is your broker leveraging the latest in benefits technology? Telemedicine, enrollment software, and a centralized benefits administration platform are all tools that can make a big difference for growing businesses.

• Do your employees report a high level of satisfaction with their benefits?

• Have your benefits expenses per employee been going down year over year? If not, your broker might not be doing everything they can to minimize your costs.

If you find that many of these questions can be answered with a ‘no’ and your broker is unwilling to adapt to meet these challenges, then it may be time to do some serious thinking. It isn’t worth staying with a broker who is underperforming and damaging your business, no matter how great your relationship with them is.

What to Do if Your Broker is Friends with Your CEO

One of the worst positions you can find yourself in as an HR or Finance professional is being dissatisfied with a broker who is buddies with your CEO or a board member. You understand what’s best for the business, but your hands are tied by your higher-ups’ relationship with the ineffective broker. How can you go about convincing them that it is time to reevaluate the relationship?

Of course, you can always send them this article. But that in itself may not be sufficient. The first thing you should do is collect as much information as you can. Research the latest benefits and technology, what other brokers offer, and what other companies pay for their benefits. Conduct employee surveys to identify employee needs and attitudes towards the current benefits. It might even be a good idea to solicit quotes from other brokers so that you can provide concrete alternatives when presenting your position to your CEO or board.

The next step is to use this information to craft a business case for switching or reevaluating brokers. Focus on ROI in terms of benefits expense savings and talent acquisition, retention, and engagement. Whenever possible, back your claims up with data. Draw a comprehensive picture of your company’s current benefits package and its performance, and then use your research to show how it can be improved.

If you draft an effective business case you will hopefully convince your higher-ups that something should be done about the company’s benefits. It’s now up to you to show them the path forward. Outline the steps involved in switching brokers (did you know that switching brokers is extremely simple?). If you’ve already gotten initial quotes, you can use these to smooth the transition to a more proactive broker. Not only will explaining the next steps help you make your case, but it also will help ensure that action is taken to remedy the situation. Companies often hesitate to take these kinds of big steps out of fear that they will disrupt the business’s operations. Laying out a clear path forward, along with its costs, savings, and effect on employee experience can make the difference between staying with your current broker and taking the next step to help your business grow and succeed.

Key Takeaways

We’ve covered a lot of ground in this article and reevaluating your relationship with your benefits broker is a highly complicated and charged topic, so we don’t expect you to have it all down right away. Feel free to refer back to this article whenever you need a refresher, and keep in mind the key points we’ve covered:

• Your employee benefits are your second biggest talent-related expense and one of your primary tools to attract, retain, and engage the talent your business needs to grow and succeed. So taking a strategic approach to working with your broker is incredibly important to your business’s health. Even if it means reevaluating your business relationship with a broker who is also your friend or family member.

• Unfortunately, brokers who you have a personal relationship with will often take your business for granted. That means that they will start providing a lower level of service, fail to update your benefits, and not work as hard to minimize your costs while maximizing value for your business.

• It’s a good idea to make an objective evaluation of your current broker so that you can get them to deliver better results for your company and its employees or so that you can find a more proactive broker.

• If you’re ready to change brokers but your higher-up has a relationship with the existing broker, then you need to craft a business case for switching brokers using as much data as you can collect, and you should outline the steps necessary to change brokers.

Your benefits broker has too much power over your business’s long-term success for you to rely on the same broker based on a sense of obligation due to your existing relationship. Reevaluating that relationship will allow you to maximize the value for your business and its employees, whether you change brokers or not.

Businesses are only as good as their best assets. It may sound like a greeting card sentiment, but it’s absolutely the truth.

Hiring the right people shouldn’t be your only concern. In any industry, growth and success are only possible when top talent is fully bought-in and authentically motivated. That means that maximizing business returns requires an intentional strategy to ensure that smart, talented professionals see the incentive in working up to their superstar potential on a yearly, quarterly, and daily basis.

Cash bonuses are a classic way to reward and motivate employees around the holidays or at end-of-year, but they can also be incorporated as part of a regular employee engagement and retention strategy that helps top talent buy into your culture and maximize their work hours to deliver business-growing results.

In this article we’ll cover:

● Why cash bonuses are so powerful

● Why cash bonuses aren’t just for big, established companies

● Ways businesses can create an effective, fair cash bonus strategy

The Power of Cash

Cash is a powerful motivator. At the end of the day, it’s why most people go to work. Unfortunately, though, life gets in the way, and thanks to bills and other financial obligations, very few professionals feel like they’re ever able to fully enjoy the salary they earn.

More than ever, young professionals with impressive talents are also managing impressive debt. For many 35 and under, getting the right qualifications and building their skill set required $100,000 or more in student loans. That’s why, unlike any generation before them, rising millennial executives and top Gen Y talent often live bill-to-bill and paycheck-to-paycheck in a way that was previously associated with blue collar work.

Cash-strapped anxiety among white collar professionals isn’t limited to young talent, however. Increasingly, senior executives and professionals beginning to eye retirement must choose between today and tomorrow, finding themselves forced to either wear the belt tighter than ever in the closing years of their careers or risk outliving their retirement savings.

Most HR directors have recognized these emerging trends over recent years, but few businesses have articulated a strategy for alleviating these stressors. Salaries cover the bills, but can employees really be expected to do their best, biggest, most impactful thinking and work when they’re just covering the bills? Can innovation at the business or national level continue when people feel like they’re barely scraping by?

Pushing talented professionals at both the leadership and individual level requires genuine incentive, and in the current climate, cash is the greatest possible incentive.

Cash bonuses invite employees to make the purchases they want, not just the purchases they need, and get a direct, powerful snapshot of how their effort and hard work directly result in money and buying power. Whether it’s upgrading the TV, pulling together a down payment for a house, or planning a family vacation, a cash bonus at the right time can provide a significant lifestyle upgrade or a major weight off the shoulders.

While salary, benefits, and even equity show employees how they are valued in the talent marketplace, bonuses help them see how they are appreciated by their current employer. A timely cash bonus illustrates both company satisfaction with current performance and commitment to the worker’s long-term fluidity. This helps build the degree of buy-in that pushes brilliant minds toward innovation and profitability.

In the current climate, top talent is presented with more chances to switch teams and explore new opportunities than ever before. Maintaining a strong, highly motivated team requires providing compensation that doesn’t just work for employees but actively makes them feel good at what they do and the culture of the place in which they work.

Too often, people have mischaracterized cash bonuses as “buying loyalty,” but the fact of the matter is that in a diverse, competitive talent market, it is the employer who needs to demonstrate loyalty in order to maintain their top rising talent and motivate them to grow with the business.

When faced with the option of continuing at a company that offers cash bonuses, moving to a parallel role at a new employer that does not offer cash bonuses, or transitioning toward freelancing/consultation, there’s simply no question which situation the compensation-minded employee will choose, especially if they have a TV, house, or seat at a private school for their child that a bonus helped them afford.

Aren’t Cash Bonuses Just for Big Companies?

While many employers provide informal holiday or end-of-year bonuses, few have a clear, consistent cash bonus strategy. That’s in part due to the misconception that in order to offer employees a lump cash sum above their salary, you need a Fortune 500 bank account. In fact, lots of small and medium-sized businesses have never even considered offering regular cash bonuses because they’re not sure they can afford it.

Actually, well-scaled cash bonuses are one of the most effective ways small and medium-sized businesses can push their top talent to achieve and make themselves stand out compared to the competition. Bonuses feel especially impactful on a smaller scale and help employees feel bought-in in a way that pushes people to work in an innovative and company-centric manner. It just requires a little more creativity to get there.

The most classic way smaller firms can provide bonuses without obliterating cash funds is to spread that bonus out over a term. For example, a hypothetical $1,000 bonus could be paid out with $500 up front and an extra $100 per paycheck for a set number of terms.

This kind of partially deferred bonus is beneficial for both talent and the employer, as the employee receives both an impactful short-term bonus and, essentially, a short-term raise, while the employer avoids depleting their cash reserves, especially in a scenario where an entire team or department is being bonused. Practices such as these can help small businesses close the cash gap and offer competitive, rewarding bonuses.

Cash bonusing is also ideal for start-up owners who prefer to maintain as much of their equity as possible. A regular, achievable cash bonus framework empowers employees to see real returns faster than in a vesting scenario, making a bonus-powered business more appealing to talent compared to similar organizations that are asking potential employees to take a five-year bet.

Anchoring a Bonus Strategy

Here’s the thing with cash bonuses: they have to be fair, transparent, and grounded in carefully measured KPIs. One of the biggest misconceptions out there is that bonuses come from a black bag of discretionary money that leaders can use to reward their favorites. Building a culture in which cash bonuses are a valuable incentive and motivator for everyone means obliterating that preconception and presenting a clearly articulated approach to bonuses that gives employees brass rings to reach for and shows them that hard work is truly rewarded.

For each asset within the organization, bonus opportunities should be tied directly to expectations laid out in their individual job description and their performance on on-going projects and initiatives. That means strengthening the connection between leadership, accounting, payroll, and HR to ensure that there’s a clear vision for each position in the company and an understanding of what adequate and outstanding performance look like in each scenario.

Ideally, employees should sign on knowing what kind of bonuses they can qualify for from the outset and what kind of data gathering and analysis leaders will conduct in order to determine their eligibility. For organizations unveiling a new bonus strategy, it’s absolutely crucial that existing employees understand which aspects of their work and KPIs are tied to bonuses and what they can do to ensure they qualify. Regular check-ins from supervisors and leaders can reinforce the company-wide culture of working toward bonuses and keep individual team members bought into the system.

When rolled out correctly, a cash bonus incentive system can give long-time talent the push they need to make it to the next level while attracting new potential superstars. On the other hand, if rollout is fumbled or articulated poorly, a seemingly unclear or unfair system can actually hurt workplace culture.

Scheduling a Bonus Strategy

Given that clarity, transparency, and fairness are so crucial to using a cash bonus system as an employee motivator and attraction/retention tool, organizations must articulate from the outset how they will schedule bonuses. Traditionally, bonuses are given on a yearly, quarterly, or project-based schedule. Let’s quickly look at each of those approaches to discuss how they differ:

Yearly: Advantages: Yearly cash bonuses have been traditional in the workplace for several centuries. Businesses can plan financially to bonus everybody at once. Workers get a large lump sum.

Disadvantages: A year is a long term, which means assessment is complex for leadership and bonuses are fewer and further between for workers.

Quarterly: Advantages: Business planning and accounting is typically conducted in quarters. Quarterly business metrics can most directly inform bonus decisions. Quarterly check-ins with employees regarding goals and company culture feel appropriate and unobtrusive.

Disadvantages: Assessing goals and tracking KPIs for all workers on a quarterly basis is a job unto itself, potentially for more than one person depending on company size.

Project/Milestone-based: Advantages: Milestone-based bonuses reward assets directly for getting work done. They provide a timely reward and a pat on the back.

Disadvantages: It’s easier to quantify and articulate bonus qualifications for some positions (e.g. project manager, sales professional, etc.) than others (e.g. graphic designer, service technician, etc.). Mindful planning must be employed to ensure fairness in terms of assignments.

Individual vs. Group bonuses: One theme that we see across all these bonus scheduling strategies is that businesses must be mindful about whether they want to create an approach in which a large number of employees are potentially getting bonused around the same time or try to stagger assessments to provide massive cash pay-outs in a small time frame.

For smaller businesses and startups, spreading those payments out is preferable in most situations. That means staggering assessment quarters across the workforce, potentially deferring bonus payments out over a longer term, and calibrating bonus goals to be attainable but adequately lofty. All those concerns again speak to the necessity of extensive planning (both in terms of articulation and financial allocations) in the months before rollout.

Key Takeaways:

● Cash bonuses are especially relevant and attractive in a climate where many professionals are wrestling with debt or trying to secure retirement. ● Cash bonuses both attract new talent and provide current assets with the push they need to take their work to the next level. ● Businesses of any size can offer cash bonuses if they commit to a program and get creative. In fact, cash bonusing can be a good way for start-ups and smaller companies to protect equity. ● In order to work as employee motivators and attractors, bonus programs must be grounded in practices, schedules, and KPIs that are clearly codified and administered as part of a transparent system.

Are you interested in learning more about how to effectively leverage cash bonuses at your business? Don’t miss our upcoming webinar:

The U.S. job market has drastically changed in the last decade. We’ve gone from a 10% unemployment rate in October of 2009 to a 3.6% unemployment rate in April of 2019. With more jobs than people to fill them, businesses are struggling to hire. In fact, 36% of small businesses couldn’t fill their open positions as of June of 2018.

Now that it’s a candidate’s job market, it’s time for recruiters and HR departments to change the way they approach hiring. If your business isn’t creating a positive, streamlined, and modern experience for candidates, you will miss out on quality hires.

In order to attract the best candidates, you need to reinvent your hiring strategy and ditch outdated recruiting practices. That’s why we created a list of the top 5 recruiting strategies that need to go—and what you should replace them with.

1.Cold Emailing Cold emailing is one of the most outdated recruiting practices you can use. Emails have a low average open rate of 20% and a response rate of a mere 6%. In today’s job market, when professionals regularly receive unsolicited communications, they are even less likely to open your emails.

Instead of sending cold emails, ask your business’s employees to refer and connect you with prospective candidates. Candidates are more likely to respond after a personal introduction.

2. Focusing On GPA When businesses evaluate younger members of the workforce, they often look at their GPAs. In 2013, 67% of companies reported that they screen candidates this way. However, GPAs don’t measure professional experience and aren’t accurate indicators of professional success.

Instead of focusing on candidate GPAs, review critical candidate skills, such as written, oral, organizational, and any other role-specific skills your open job calls for.

3. Geographically Restricted Candidate Searches In today’s cosmopolitan business environment, geographically restricted searches are one of the most egregious outdated recruiting practices. A majority of recruiters (67%) say their biggest challenge is a lack of skilled, high-quality candidates. Searching for candidates only located within your geographic area drastically limits your search—especially if you’re looking for higher-level employees.

Unless your business is on a tight budget, you should be searching for candidates across the country. Video calls and Skype have made it easier to reach these long-distance candidates.

4. One-Way Conversations Eighty-three percent of professionals say a negative interview experience can change their minds about a role or company they once liked. Interviews can feel like trials to employees—so be sure to avoid suffocating atmospheres, rude or pertinent questions, or intimidating two-on-one setups.

Instead of providing an unnerving experience, give your interviewees a chance to respond, engage in conversation, and ask questions. Smiles don’t hurt, either.

5. Scripted Conversations The majority (90%) of millennials, who are the largest generation in the U.S. labor force, say brand authenticity is important. They feel the same about the companies they work for, too. Scripts can make an interviewer seem inauthentic and a company seem robotic—the opposite of what millennials want to experience at work.

Instead of using a script, try to make candidate conversations as real as possible. Go off script, be yourself, and have fun getting to know another professional.

Overview Many outdated recruiting practices are designated as such because of today’s new workplace standards of authenticity and positivity. In general, your business should be systematically humanizing the recruiting process to catch up with modern candidate wants and needs.

Ditching outdated recruiting practices, from cold emailing to scripts, will improve your candidate experience, widen your candidate pool, and help you fill your empty roles with high-quality talent.

About the Author Tim Schumm is the founder/CEO of Lucas James Talent Partners. Lucas James Talent Partners provides small and medium-sized businesses with a high-quality, cost-effective, and flexible talent acquisition solution through RPO (recruitment process outsourcing). Please visit https://lucasjamestalent.com/ to learn more.

Many companies stay with the same employee benefits broker just because they are afraid that switching will be too difficult. They imagine that changing benefits brokers will entail a lot of paperwork, direct communication with insurance carriers, and major changes to their insurance plans and benefits package. The disruption caused by such a shift would certainly outweigh the advantages of switching to a new broker, at least in the short-term. So they stick with the broker they know rather than working with a broker that will best meet their needs long-term.

But the fact of the matter is that it really isn’t that hard to change benefits brokers. It doesn’t take a lot of time and doesn’t require major changes in your benefits package or internal processes. So there is no reason to stay with a broker you’re dissatisfied with because you are afraid of what changing might involve. In this article we’ll address some of the misconceptions that you might have about switching brokers and outline how easy and rewarding the process really can be. The key points which we will cover in this article are:

• You can keep your insurance carriers and plans

• You can switch any time throughout the year or phase of the renewal process

• If you want to change insurance plans or carriers, the process is quite easy with the right benefits broker

• Switching benefits brokers can produce serious results for your business

You Don’t Have to Switch Insurance Carriers or Change Benefits Packages

Despite what many people think, changing employee benefits brokers does not mean that you need to change your benefits package or insurance carriers. You simply need to notify your insurance carriers that the new benefits broker is representing you instead of the old broker. You do this by submitting a Broker of Record (BOR) form to the carriers, which enables the new broker to negotiate with the carriers on your behalf, monitor rates, and advise you on the best benefits package. To make things even easier, your benefits broker can handle the process of drafting and sending the BOR, you just need to sign it.

Now, you may wonder why you would switch employee benefits brokers if you’re just going to keep the same insurance plans. But your healthcare plan is only one part of the overall benefits picture. A good benefits broker will be able to work with you to optimize your benefits package or phase in a new one without disrupting your employees’ experience or internal processes. Plus, a great benefits broker can streamline and improve the benefits experience for you and your employees within the same plan structure. They can provide increased service and support, including employee education initiatives and enrollment or benefits administration software platforms. And they can also negotiate new, lower rates for the same plans at the next renewal.

There Are No Time Constraints on Switching Benefits Brokers

You don’t have to make the switch to a new employee benefits broker at a particular time of year or phase of the renewal process. You can submit the BOR at any time and since doing so won’t require that you change your benefits package, the timing for when to change benefits brokers doesn’t depend on whether or not you’re ready to change your benefits package. Your internal processes will not have to change, and your employees won’t notice any difference in their benefits experience.

This means that you can switch benefits brokers as soon as you have found the right partner for your business. That way the new broker will have access to the information they need to start advising you on your benefits strategy and optimizing your benefits package. You can work together to craft a better approach to benefits and phase in your new benefits initiatives while providing a seamless experience for your employees.

With the Right Benefits Broker Switching Insurance Plans Isn’t Difficult

While you do not have to change your benefits package when you switch benefits brokers, you can explore options for an improved benefits package to your employees at a lower cost to the company. This may sound daunting, but it’s really not very difficult or even that time consuming when you partner with a strategic-thinking, proactive benefits broker.

Don’t get us wrong, switching plans does require a slightly longer transition period, but it’s still not that complicated relative to renewing your existing plans. Plus, most of the work will be handled by your benefits broker.

The first thing that your new benefits broker will do is take a census of your employees to collect the information that they need to assemble your new benefits package. Then they will send out an RFP and collect proposals from different carriers to provide you with the best possible options to choose from. Or, if you have established carrier relationships and preferred plans, they will get an updated quote based on your specific needs and your employee data.

Once you and your broker select a carrier, it’s time to enroll your employees in their new insurance plans. Now, the words “open enrollment” might send most HR professionals running for the hills, but a good broker will actually make this process painless. Many benefits brokers will provide centralized platforms for employees to view and enroll in plans and for your HR team to store data to monitor compliance. And boutique benefits brokers will work directly with your employees to educate them about their new insurance options and the enrollment process in general.

At the end of the day, if you’ve picked a great benefits broker, your role in the transition to a new benefits package will be minimal.

Switching Benefits Brokers Can Reap Real Rewards for Your Business

Not only is switching brokers a lot easier than people expect, but it can also be seriously important to your business’ success. According to a Met Life survey, 76% of employers believe that brokers help them get the best possible prices on employee benefits, and nearly as many say that their brokers help them to stay compliant. If you don’t feel like your broker is doing enough to help minimize your costs, maintain compliance, and provide the best possible benefits for your employees, then switching is well worth the minimal inconvenience.

The fact of the matter is that benefits spend is a huge part of your overall budget and makes up 25-40% of most companies’ payroll. So it’s important to work with the right partner to minimize those expenses while maximizing the return-on-investment of the remaining expenses. For instance, a great benefits broker will reduce your benefits costs by strategically designing plans that are the right fit for your employee demographics and helping employees become better consumers of their healthcare. They can also reduce costs by introducing discount prescription drug plans, technological solutions like telemedicine and wellness programs that help prevent long-term expenses from lifestyle diseases.

More importantly, your benefits package is one of the greatest tools in your arsenal to attract, retain, and engage great talent that will help your business grow and succeed. According to an Aflac survey, 80% of employees believe that their benefits package influences their engagement in their jobs. In addition, most said that they were likely to accept a job with lower compensation and better benefits. Clearly, compelling benefits are essential to any effort to attract top talent as well as maximize employee productivity and retention.

Your new broker will be able to provide the best possible package for your employees by conducting third-party surveys to identify their needs and then crafting a benefits strategy to meet those needs. All while reducing costs by eliminating benefits that your employees don’t need or want.

Finally, if you pick the right benefits broker, they will see each of your employees as their clients, rather than just focusing on appeasing your company’s top executives. These benefits brokers will work on the individual employee level through seminars, Q&A sessions, and other forms of direct communication. This hands-on approach will help employees understand how to navigate the benefits package and make the most of the benefits offered. It will also impress upon employees the value of the benefits in order to maximize the impact that your benefits have on employee retention and engagement.

Key Takeaways

Changing employee benefits brokers may seem like a very daunting decision, but the actual process of making the switch once you have found the right benefits broker is surprisingly easy. Plus, with so much on the line when it comes to your employee benefits package, the minimal amount of effort required is well worth it. Because at the end of the day:

• You can keep your insurance carriers when you change your benefits broker

• You can change benefits brokers any time or phase of the benefits renewal process

• Switching insurance carriers is quite easy with the right benefits broker

• Your benefits broker is responsible for managing up to 40% of your payroll costs, so make sure you’re partnering with the right broker for the most cost-savings and best return on your benefits dollars invested

So switching brokers isn’t that difficult, but you do need to find the right partner. Want to make sure your current broker is serving your needs? We wrote a handy article that will show you how to evaluate your existing broker. Check it out right here.

Launchways, a leading provider of human resources, employee benefits, and business insurance solutions today announced that it is taking on Paycor, a comprehensive HR software provider, as its latest strategic partner.

As a strategic partner, Paycor will work with Launchways to deliver meaningful content that helps guide CFOs in the world of HR. In many growing companies, financial leaders are finding themselves taking on responsibility for the human side of their organization. Through this partnership, Paycor and Launchways hope to help guide CFOs through people leadership best practices.

Paycor’s mission is to provide business leaders with the tools they need to empower their workforce. Their Human Capital Management platform streamlines key HR processes so that executives, HR professionals, and employees can focus on what really matters: building real human connections and fostering innovation.

“Paycor’s vision aligns perfectly with Launchways’ values, and we’ve collaborated frequently in the past. This commitment will help take our partnership to the next level” said Launchways CEO, Jim Taylor. Launchways helps businesses build strategic HR infrastructure and employee benefits programs that scale as the company grows in order to unlock the full potential of their workforce.

“At Paycor our top guiding principle is taking care of our clients. Through partnerships like Launchways we’re not only able to provide best-in-class human capital management technology, but share valuable thought leadership to help clients stay ahead of HR trends. We look forward to working with Launchways to continue providing unparalleled support to our joint clients” added Bob Balogh, Vice President of Channel Partnerships at Paycor.

Establishing effective, efficient HR systems that scale with the company as it grows can be a significant challenge to CFOs who find themselves taking on HR leadership roles. Through their partnership, Paycor and Launchways aim to make the process easier for finance leaders, especially in fast-growing technology companies.

About Launchways

Launchways provides business leaders with the resources and guidance they need to build scalable people processes to support long-term growth. Founded in 2009, Launchways has helped hundreds of growth stage businesses better approach the people side of their business through strategic solutions for human resources, employee benefits, and business insurance. For more information, please visit www.launchways.com.

About Paycor

More than 30,000 small and medium businesses nationwide trust Paycor to help them engage, manage and develop their people. Paycor is known for delivering the best unified HCM platform for the SMB market, but what makes us legendary is the total customer experience we provide, from responsive service and user-friendly design to expert partnership and thought leadership. Our unique combination of technology and expertise helps clients streamline every aspect of people management so they can focus on what they know best—their business and their mission. To learn how Paycor can help you make a difference, visit www.paycor.com.

Last week Launchways collaborated with FinTex to host an educational panel which focused on the HR issues startups face as they scale. FinTex is a nonprofit organization which provides local Financial Technology (“fintech”) startups with the education and resources they need to be successful. Having identified HR issues as a top challenge area for the Chicago fintech community, FinTex enlisted Launchways to host an educational event on the topic.

Launchways is a Chicago-based provider of strategic solutions for Human Resources, Payroll, and Employee Benefits. Launchways specializes in working with growing companies to help them get the people part of the business right. As a member of the vibrant Chicago startup community themselves, Launchways was elated by the opportunity to partner with FinTex to support their mission of educating local fintech leaders.

Launchways assembled a panel of expert HR thought-leaders representing some of the fastest growing companies in the Chicago fintech space. Panelists included:

Ryan Pollock, Managing Partner, Objective Paradigm

Carolyn Kwon Montgomery, VP of People, Pangea Money

Carrie Gibson, Head of Talent Development Diversity & Inclusion, Avant

Launchways was also excited to welcome Jay Rudman, CEO, TopstepTrader, who gave the opening remarks at the event and is an active leader with the FinTex organization.

Launchways CEO, Jim Taylor, introduced the panelists and moderated the discussion throughout.

The topics covered during the panel included:

Recruiting: high-impact recruiting strategies and tips on how to create seamless hiring processes to build your team as you grow.

Retention: how to audit your company’s employee retention health and enact effective strategies that engage and retain your key employees.

Compensation/Equity: how to structure effective compensation packages and better understand how to reward and retain key employees with equity.