Amid legislation that pushes consumerism in healthcare while putting greater burdens on healthcare consumers, employers and employees alike have turned to high-deductible health plans (HDHPs) to minimize their healthcare costs. As premiums continue to rise, these plans offer an opportunity to keep upfront costs low for companies and their employees. At the same time, the IRS permits the creation of tax-exempt health savings accounts or HSAs for people with HDHPs to cover the costs of the higher deductibles when expenses do come up.

This system works great for everyone involved – so long as people stay healthy. Which makes preventive care an integral part of any successful HDHP based healthcare strategy. By allowing patients to head off health issues before they become significant expenses, preventive care keeps everyone’s expenses down and maximizes health outcomes for the insured. Recognizing this, the IRS has allowed insurance plans to cover preventive care such as check-ups, screenings, immunizations, and tobacco cessation or weight-loss programs with a low or non-existent deductible while keeping their HDHP status.

However, the IRS has not generally extended the same low-deductible permissions to treatments for existing illnesses or conditions. Since 2004, certain on-the-spot treatments for conditions discovered during screenings (such as removing polyps discovered during colonoscopies) and medications to prevent recurrence of heart attacks or to reduce cholesterol to prevent heart disease have fallen under the umbrella of preventive care, but that’s about it.

Which means that people with chronic conditions have generally been left out. They have had to choose between paying out high-deductibles for treatments that prevent their conditions from worsening, or giving up their HSAs and adopting high-premium plans. Until now, that is.

The IRS’ New Rule

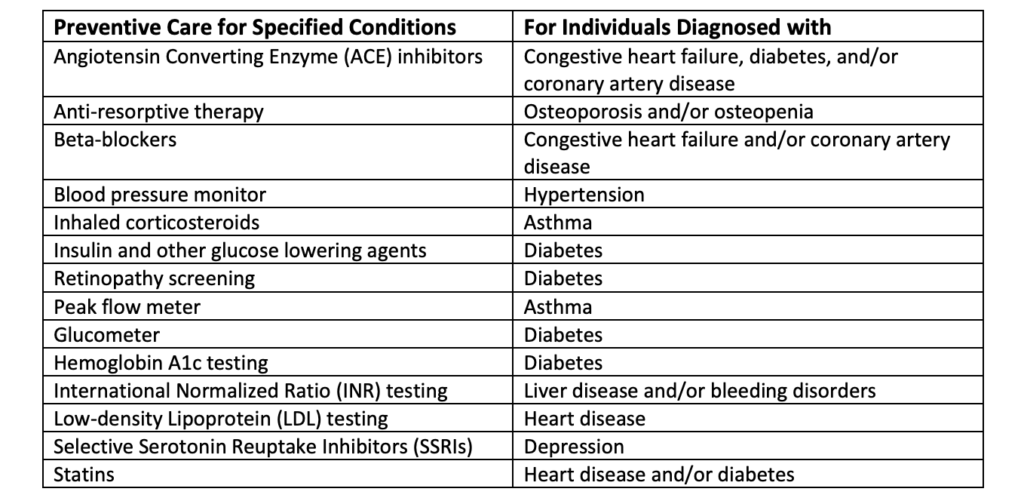

On July 17, 2019, the IRS issued Notice 2019-45, which significantly broadened the definition of preventive care to extend it to many treatments for chronic conditions. To qualify as preventive care, the treatments must be likely to prevent the worsening of a chronic condition or the development of a secondary condition which would incur greater healthcare costs. It must also meet several other criteria, which we have outlined in this handy chart for easy reference:

The Impact for Companies and Their Employees

So what does this policy change mean for employers and employees? Simply put, it provides enormous opportunities for both to take greater control over their costs, minimizing their expenses while maximizing employee health and wellness. It makes the already appealing HDHP and HSA healthcare option a win for employees who want to increase their welfare and for employers who are looking to reduce their expenses.

The expanded definition of preventive care provides a new opportunity for employers to educate their employees so that they can become more intelligent consumers amid government policies which force consumerism in the healthcare market. Employees can use HDHPs to control their costs without fear of compromising their health, especially by neglecting chronic conditions to avoid paying high deductibles. Instead, they can get the treatment that they need at low costs while keeping their tax-exempt health savings.

Key Takeaways

We’ve thrown a lot of information your way in this article, so here are some key takeaways that you should remember:

• IRS Notice 2019-45 opened up serious opportunities for employers to cut their costs and for employees to reduce their expenses and maximize their healthcare outcomes

• Chronic conditions will no longer force consumers to take on significant healthcare costs to receive the treatment they need to maintain their health and avoid future expenses

• That means that high-deductible health plans, which already provided the best solution for consumers in the current healthcare market, are now better than ever

To make the most of the rule change as an employer, you should partner with a proactive benefits broker who will help you craft a healthcare strategy which maximizes the impact for your employees while minimizing your costs. Benefits are an important tool to attract, retain, and engage the talent that you need to grow your business. The well-being of your company and its employees ultimately depends on the effectiveness of your benefits strategy. So it is more important than ever to work with the right benefits broker.

Interested in making the switch to a broker who is invested in your growth and your employees’ well-being? Start the conversation today.