At Launchways, we’re constantly looking for new innovative, effective ways to help businesses meet their HR, employee benefits, and business insurance needs. This month, we’re proud to announce we are adding Group Insurance Captive solutions to our ever-expanding portfolio of solutions for growing businesses.

In this post we’ll:

Define Group Insurance Captives in a straightforward and useful way

Explain the value proposition of our group captive membership

Describe why we’re so excited to be offering this new program

Provide next steps for businesses hoping to learn more about our group insurance captive

What is a Group Insurance Captive?

A “captive” insurance company is an organization founded with the sole purpose of providing business insurance to its owner(s).

Essentially, a captive is the purest form of self-insurance. A business or group of businesses forms a captive in order to meet their insurance needs without being beholden to the packages, limitations, and pricey markups of the traditional marketplace.

A group insurance captive specifically involves a group or “pool” of businesses with similar scales or goals coming together to create and share a captive insurance company. That new company, managed by a designated third party, obtains insurance for each owner/member organization, processes their claims, and maintains the overall health of the pool.

How Do Businesses Benefit from Joining Our Group Insurance Captive?

So, now that you know what a group insurance captive is, the natural question is: Why would you want to be part of one?

Organizations that form or participate in a group captive have greater independence, greater power for self-determination, and greater potential for profit. Let’s take a look at some of the specific ways those gains play out:

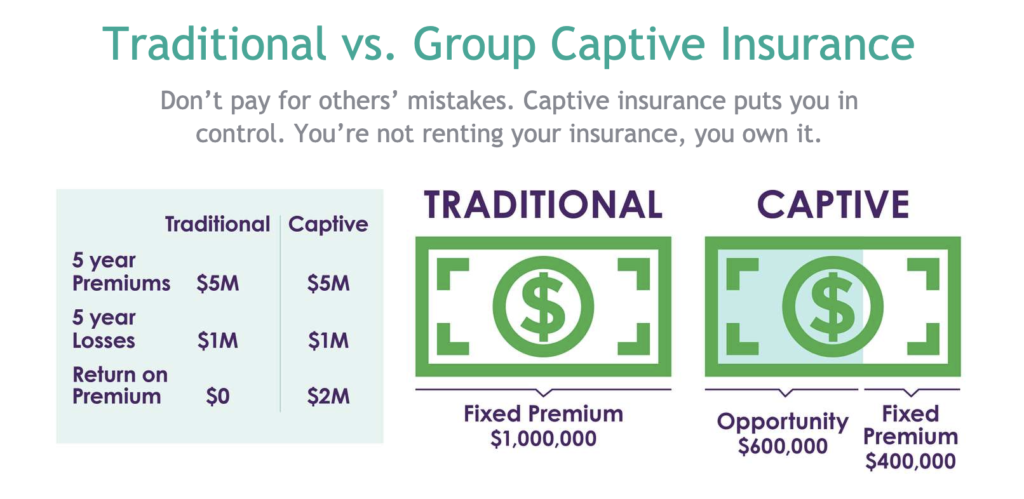

In the traditional marketplace, you rent your insurance. With a captive you own it.

Total continuity of services as desired

No stress over price-gouging at policy renewal

In the traditional marketplace, business insurance is an expense; in a captive, it’s an opportunity for return.

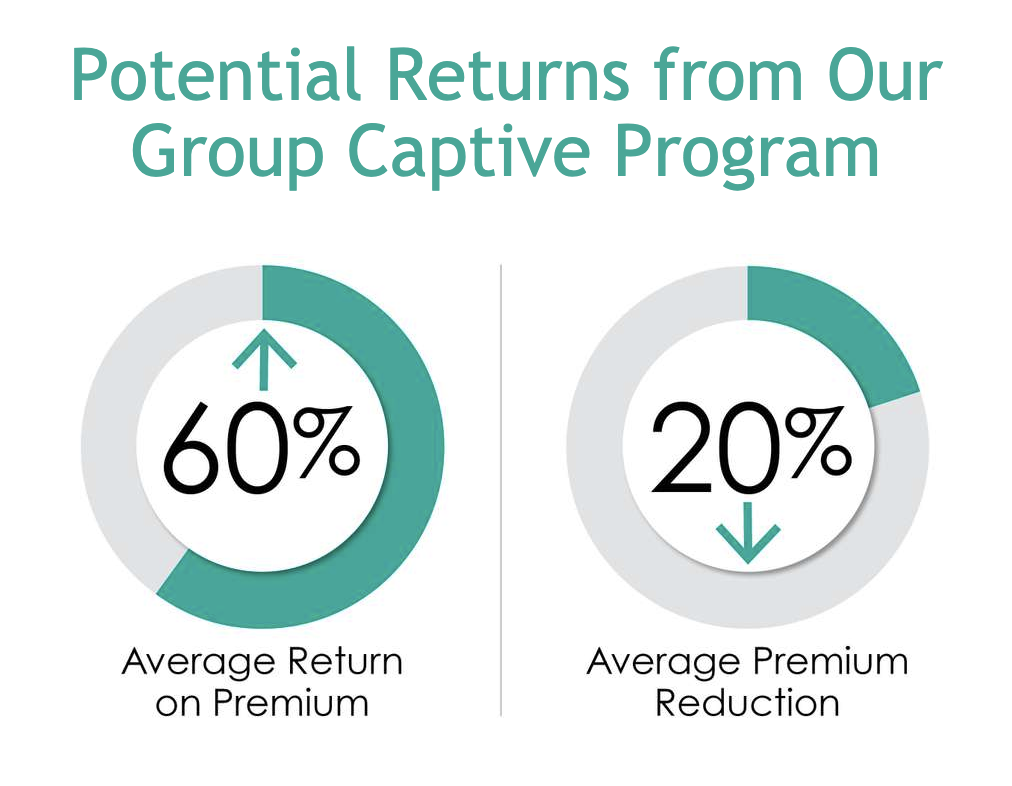

Get up to 60% average return on premium

Use safety initiatives/risk management skills to maximize your payout

With your own insurance company, you can get exactly the coverage you need and eliminate overspend.

No more bundled services you don’t want or need

Turn self-knowledge into efficiency-of-scale

Owning your insurance company means you call the shots!

Work with your pool partners to set the tone for the captive

No more getting sold out or let down by the insurance company

With a captive, you have greater access to insurance data than ever before.

Understand your needs, claims, and expenses better than ever

Gain insights to help streamline coverage/claims processing in the future

How to Know if You’re a Good Fit for Our Group Insurance Captive:

Once you hear about the potential benefits of group insurance captives, it’s natural to wonder if your organization is a fit to join.

If your business can answer “YES!” to each of the following questions, then you’re a great candidate for our new group insurance captive program:

Do you pay $150,000 or more in insurance premiums each year?

Does your company have an entrepreneurial spirit?

Does your company desire greater control and stability?

Does your company understand the concept of “risk for reward?”

Is your company committed to safety?

Why Join a Launchways Group Insurance Captive in 2020?

Now that you’ve got a general understanding of what group insurance captives are and what kind of value they offer businesses, it’s time for us to answer another important question: Why us?

Since our inception, Launchways has focused on providing support and solutions that help growing businesses thrive in the immediate future while also planning for long-term success.

We’re entering the world of Group Insurance Captives because we understand that business insurance needs are increasingly diverse, and more and more organizations are feeling frustrated by the limitations of the traditional marketplace. We want to help our clients bet on themselves, forge powerful partnerships with likeminded businesses, and get the exact coverage they need to thrive.

We believe in the power of growing organizations to improve the business space and lead the next wave of American innovation. That’s why we’re helping businesses find potential pool partners, organizing our group insurance captive, and connecting organizations with the management and expertise they require to ensure their captive experience is successful.

Takeaways:

Here at Launchways, we’re excited to be helping our clients gain the power and freedom group insurance captive membership can bring. We’re looking forward to applying our innovative approach and emphasis on specific customer goals to help businesses gain the power, efficiency, and profit potential our group captive offers.

Remember:

Group insurance captives offer businesses true ownership over their insurance, enabling:

New profits from return on premiums

Increased control over claims management

Innovative partnerships with pool peers

To be a strong group captive candidate, a business should pay at least $150,000 in annual insurance premiums and be a stable but innovative organization

Captive insurance programs enable businesses to reduce their

insurance overspend, fully control their coverage, and turn safety initiatives

into profitable returns.

Unfortunately, though, many organizations shy away from

forming or joining captives because, when they start doing online research,

they often run into incorrect and damaging myths about captives.

Moving forward, we’ll:

Identify the top five myths about captive

insurance programs that are prevalent on the web

Debunk each myth using evidence

Describe the true value and possibilities of a

captive insurance program.

Myth #1: You have to be a huge corporation to benefit from a captive

Why is this myth so prevalent?

When you first start researching captive insurance programs,

most of the messaging on the first page of search engine results focuses on how

captive programs are used by large corporations who hold multiple businesses

and operate facilitates across the globe.

Why is this a myth?

It’s true that single-member captives (in which one business

creates its own insurance company) are generally formed by large corporations,

but that’s not the full story! Group insurance captives or “pool” captives

specifically exist to bring together medium-sized businesses so they can gain

the insurance negotiating power of their bigger competition.

When it comes to whether or not your business is a good

candidate to join a group captive, your business’ size, headcount, or profits

don’t enter into the equation at all. It’s all about the scale of your business

insurance premiums.

The Bottom Line

If you pay more than $150,000 annually in premiums, you are

a strong captive pool candidate. You don’t need to be a multi-national

corporation or a Fortune 500 giant – just a business with a goal of doing

things better.

Myth #2: Entering a group or pool captive exposes your business’ health to

other people’s risks

Why is this myth so prevalent?

The idea that group insurance captives expose your money to

other business’ risks is a logical fallacy. That is, it seems right on its

surface when you have a cursory knowledge of the topic, but a deep dive proves

it to be completely false.

When businesses hear the words “group” and “insurance”

together, they incorrectly assume risk and responsibility are shared equally

among the pool members for claims. They connect the dots and assume that if one

pool member has a “bad year,” it damages their business allies as well.

Why is this a myth?

Pool captives are specifically structured to protect the

vast majority of each member’s investment from the risks and claims of others.

Over 90% of your premiums are specifically set aside for your use.

That means less than 10% of your total investment can be

lost due to claims made by other members of your pool.

In fact, in Launchways’ group captive program, each member retains complete ownership of 98% of their funds. This means that with the Launchways group captive, only 2% of your investment is considered “at-risk.”

The Bottom Line

Yes, group captive membership requires the willingness to

take on increased risk compared to the traditional insurance marketplace, but

it’s absolutely false to say that your potential for profits is at the mercy of

your pool partners.

Myth #3: When you’re in a captive, one big claim can blow up your business

Why is this myth so prevalent?

Like Myth #2, the “catastrophic claims scenario” is a

logical fallacy: it sounds right, but it isn’t! When people hear “self-insurance,” they assume

that means “we’re on the hook for every dollar and cent of every potential

claim.”

Unfortunately, this myth is also sometimes perpetuated by

insurance providers and brokers who are hesitant to work outside the traditional

marketplace. Their motivation is to protect their own interests and ease of

doing work, not yours!

Why is this a myth?

One word: reinsurance. Whether you operate your own

single-member captive or participate in a group or pool program, part of your

investment is always in reinsurance to prevent exactly this scenario.

That reinsurance policy prevents unforeseen or

much-larger-than-expected claims and issues from damaging your business’

long-term viability or standing as a strong group captive partner.

The Bottom Line

Reinsurance is a part of every captive program, and it’s

there to protect you from potentially harming the health of your business.

Myth #4: We’d have to change the way we do business to form or join a

captive

Why is this myth so prevalent?

The idea of creating your own insurance company sounds

pretty daunting at first. Many people assume they’ll need to restructure their

organization to make the captive viable or transform themselves into a more

attractive group pool member.

Like so many other myths we’ve tackled, this one is at least

in part in heavy circulation because many insurance package providers aren’t

crazy about the idea of businesses cutting them out as middlemen.

Why is this a myth?

The whole point of a captive insurance program is that it

allows your business to be itself more fully – you gain the ability to insure

outside-the-box risks, gain ownership over the claims management process, and

reclaim power and autonomy that traditional business insurance limits.

Captive insurance programs aren’t about changing your

business, they’re about changing the circumstances under which you do business.

Furthermore, in the case of group captive programs, independent managers handle

pool responsibilities, meaning there’s minimal change to your day-to-day

operations and responsibilities.

The Bottom Line

A captive is about supporting your business better and

providing greater economy of scale. The idea that you need to significantly

“whip yourself into shape” to be a captive candidate is false.

Myth #5: Captive programs used to offer great perks, but the value isn’t

there anymore

Why is this myth so prevalent?

Anytime people perceive the value of a product or service

has been reduced even a small fraction, there’s often an impulse to throw out

the baby with the bath water.

Single-member captive programs used to offer large

corporations significant benefit as tax shelters, and it is true that most of

those incentives have been removed. In reactionary style, many of the big business

blogs have published content claiming captives “aren’t what they used to be.”

Why is this a myth?

As we’ve established repeatedly in our myth-busting

exercise, insurance captives aren’t just for the biggest companies in terms of

workforce or economic power. Just because those industry leaders are upset about

changing regulations, doesn’t mean you should be tricked into thinking like

them.

In fact, some of those same regulatory changes that have

made captives slightly less profitable for large, multinational entities have

actually made it easier for medium-sized businesses to form effective

pool captives. Even if captives have slightly declined in value for the biggest

business, they’re still loaded with potential for mid-sized businesses.

The Bottom Line

Captive insurance programs still offer tremendous value:

independence, authentic ownership of your business’ insurance and claims

process, and the potential to make a dividend instead of turning overspend into

loss are just three examples of why they’re still relevant and extremely

useful. Don’t be scared off just because they’re not the big-money tax shelter

they used to be.

Key Takeaways:

As we’ve seen, captive business insurance programs (both

single-member and group or pool) allow organizations to navigate the insurance

market in a more personalized, powerful manner.

Even though most entities aren’t big enough to pull off a

single-member captive, medium-sized businesses are increasingly forming

alliances that provide big value and the potential for profit.

There are plenty of myths out there about captives, most of

them designed to make the programs seem scary and risky, but it’s important to

remember:

You don’t need to be a gigantic corporation to qualify for a group or pool captive – you just need to pay at least $150,000 in annual premiums

Within a group insurance captive, over 90% of your investment is protected and sequestered for your use only

Reinsurance is built into captive programs to prevent catastrophic claims events

Captives should be about enabling you to do better, not forcing you to jump through hoops

Even if they’re not spectacular tax shelters anymore, there’s still immense value in the independence and negotiating power captives create

Captive insurance programs have been popular among business’

largest corporations since they were first created in the 1950s. As we enter

2020, however, captives are enjoying a resurgence as a growing solution for

businesses of all sizes trying to think outside the box.

Captives allow businesses to maintain direct control of

their insurance programs, creating a fully personalized experience with its own

unique challenges and opportunities for reward.

Even though captive insurance programs can help businesses

navigate the challenges of employee benefits management, reduce costs, and

build a more useful experience for employees, there’s a major lack of

understanding about what they are and how they work.

Moving forward, we will:

Define captive insurance for beginners

Explain the difference between a captive and

traditional commercial insurance

Review the main pros and cons of captive

insurance

Provide guidelines to help determine if a

captive insurance program might be right for your business

What is Captive Insurance?

A “captive” insurance company is an organization that exists

only to meet the specific insurance needs of its member/owners. That means the

business or businesses insured by the captive are its sole and total owners.

Captive insurance can help a business fulfill all its

insurance needs, from employee benefits and general business insurance to worker’s

compensation, product liability, auto insurance, and so on. That’s why captives

have historically been popular with Fortune 500 companies and major

corporations: they provide complete independence and allow businesses to

circumvent many of the inefficiencies of the commercial insurance market.

When you have an insurance company whose only focus is the

support of your business, you can achieve some pretty impressive stuff.

You can get your employees the benefits plans

they need while controlling expense for them and the business

You can scale your coverage to your exact needs

to minimize overspend

You can eliminate the offerings you don’t need

while finding the best version of what you do need

In order to gain that independence, however, you must assume

the possibility of greater financial risk. When you make the switch to captive

insurance, you’re gambling with your own money, and no longer have your insurance

provider to fall back on because you are now the provider.

Different Types of Captive Insurance

It’s important to know that there’s more than one kind of

captive. Let’s take just a minute to define the main types of captive insurance

programs out there.

Single-Parent or Pure Captive: A captive

that is owned by and works exclusively for its parent company and its

subsidiaries (as for a corporation)

Group or Association Captive: A captive

insurance program created by multiple small or medium-sized companies pooling

their resources and risk to access the advantages of a captive

Rental Captive: An existing, independent

captive operated by a business entity that other organizations can opt into

temporarily

Protected Cell Captive: A captive in

which each organization’s assets and liabilities are kept separate, allowing

access into the captive but minimizing the biggest possible financial gains and

losses

Agency Captive: A captive managed by a

specific agent, who is empowered to reinsure the company by contracting with

traditional carriers based on their assessments

How is Captive Insurance Different from Commercial Insurance?

Now that we’ve defined “captive,” let’s explore how captive

insurance is different from many of the other models you might be familiar

with.

What’s the Difference Between Captive Insurance and Being Fully Insured?

In short, a captive is the complete opposite of being fully

insured.

When you’re fully insured, you pay a set monthly fee to your

insurance company and they assume all financial risk. Being fully insured is most

useful if you don’t have the capital available to cover anticipatable risks.

A captive is only possible if your business has more than

enough capital available to cover anticipatable risks or if you partner with

other organizations to pool resources.

What’s the Difference Between Captive Insurance and Being Self Insured?

Captive insurance is a form of self-insurance, but the two

terms are not interchangeable.

A self-insured business maintains a specific savings account

for unforeseen insurance costs and uses that “rainy day fund” to cover losses

or fill gaps in coverage. However, that coverage is still purchased through the

traditional insurance marketplace.

A captive is far more complex than basic self-insurance because

it involves an organization creating its own insurance entity, not simply socking

away money to pay for insurance-related costs.

What’s the Difference Between Captive Insurance and Mutual Insurance?

In a mutual insurance company, the provider is owned by its

policyholders, acts on their collective best interests, and distributes any

profit through either lower rates or payouts.

That sounds pretty similar to captive at first, but there’s

one key difference: a mutual company, although owned by its policyholders

financially, acts as an independent entity. Policyholders buy in and then trust

the provider to do good by them.

In a captive, the insurance company is part and parcel of

the greater organization which it serves and is steered according to identified

business needs.

Advantages of Captive Insurance

We’ve laid out a lot of information about what captive

insurance programs are, how they work, and how they can transform an

organization’s approach and identity. Let’s pause to reflect on the positive

potential of captives.

A captive insurance program can help you:

Reduce

insurance costs – When you own the insurance company, there’s no mark-up

for services and no need to purchase any coverage you don’t want or need.

Captives offer businesses the best and most granular control over their costs

compared to any other insurance model.

Reward

yourself for good planning – Captives provide the most benefit to

businesses with great self-knowledge. If you understand your assets, risks,

needs, and scale well, you can create a captive that protects you with minimal

overspend in a bad year and generates difference-making profit in a good year.

Create

ideal employee benefit packages – Each workforce has its own specific,

identifiable healthcare and employee benefit needs. Unfortunately, even with a

great broker, it’s tough to create bespoke coverage that meets everybody’s

needs and saves everybody money. A captive allows businesses to get creative

and find new ways to get their employees exactly what they need without having

to spend a dime on things they don’t.

Insure

outside-the-box risks – Sometimes an organization needs to take a big risk

and gamble on itself to take the next step. Finding insurance to protect

investors and keep the core of the business whole should one of those major

strategic gambles fail is more difficult than ever on the open market. If you

have a captive insurance program, however, you can create whatever coverage you

need and avoid needing to “sell” a carrier on your business plan.

Specific

tax benefits – There’s a misconception that all the tax benefits of captive

programs have been eliminated over the last few years, but that’s actually not

true. First of all, all premiums an organization pays to its own captives are

tax deductible. Furthermore, in down years, he captive’s status as an insurance

company can earn its parent organization loss reserve deductions.

Disadvantages of Captive Insurance

Of course, as we’ve seen, the captive program approach isn’t

right for every business. Let’s pause briefly and reinforce the main reasons

and organization would not want to create a captive.

Unfortunately, with a captive insurance program, you:

Assume increased risk – When you form a

captive program, you are your own support system. There’s nobody else paying

into the pool of funds that’s used to bail you out in a pure captive, and even

in a group captive, if multiple partners have bad years, it can lead to major

financial complications. If your business is risk-averse by nature, a captive

might not be right for you.

Take

on up-front expense – Establishing a captive is a time-consuming process

that requires creating an insurance company from scratch.That means, as

you’re planning and building your program, you’ll need to take on more hires,

acquire new licenses, and bring in some consultants who are captive experts. At

the same time, you need to allocate capital to underwrite your plans.

Create new management responsibilities – People

sometimes misunderstand that a captive can be managed by a human resources

department’s employee benefit expert. That’s actually not true, as the captive

is a full-time, constantly operational insurance company. That means either

bringing in new managers to operate the division or creating new

responsibilities for other members of your core team.

Risk taking a step back –It’s possible

that, in its initial years, your captive might not do as good of a job as a

traditional provider. If you’re not comfortable taking one step back to take

two steps forward, a captive probably doesn’t fit your leadership style.

Don’t

get the tax benefits you would have in the past – While captives still

deliver some tax perks, they’re definitely not the shelter and deduction

powerhouses they used to be. With that said, if your main motivation for

creating a captive is tax protection, you’re likely not a good candidate for a

captive program in the first place.

How to Know if Captive Insurance is Right for You

In general, captive insurance is best for businesses that

are:

Large and stable (or medium-sized and stable,

backed by a group of similarly stable partners)

Comfortable taking risks with the potential for

high reward

Thinking and operating in an open-ended,

creative way

Recruiting a diverse workforce with varied

medical needs and preferences

Dissatisfied with traditional corporate and

business insurance

Confident in their ability to improve over time

On the other hand, businesses should keep away from captives

if they are:

Small or in an early developmental stage

Risk averse or unable to raise significant

capital

Relying exclusively on outside companies and

contractors to identify and manage their insurance needs

Completely satisfied with the pricing and

coverage they get through traditional insurers

Unwilling to take one step back in the short

term in order to take many steps forward in the long term

Key Takeaways

Captive insurance programs are unique, complex, and create

brand new challenges for the businesses who decide to leverage them.

At the same time, however, captives remain underappreciated

as ways to meet all of your business’ total insurance needs while controlling

costs and connecting with your ideal coverage.

There’s no “right answer” when it comes to whether captive

insurance programs are effective or not; the approach’s potential for success

is directly tied to an organization’s desire to think and work beyond the

limitations of the traditional marketplace and commitment to getting things

right.

If you’re wondering if a captive program could benefit your

organization, remember:

Captive insurance companies support only the

organizations that own them

A “pure” captive involves just one company or

corporation

A “group” or “association” captive involves a

group of businesses banding together to share risk and support one another

Starting a captive insurance program is

basically the opposite of being fully insured – you assume all risk

Captives can help organizations build bespoke

insurance plans, both for business needs and employee benefits

Captives aren’t for small or risk-averse

businesses