Just before midnight Wednesday night, the Senate passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The Act creates further economic protections for individuals and businesses in addition to the FMLA and paid sick team leave expansions created by the Families First Coronavirus Response Act.

Generally speaking, CARES strengthens the safety net of unemployment insurance, offers new tax credits for businesses and individuals, and creates an emergency lending fund of more than $450 billion for businesses and municipalities.

In this post we’ll explore:

- Additional unemployment protections for individuals under CARES

- The employer-facing tax credits created by CARES

- The employee/individual-facing tax credits created by CARES

- How CARES enables emergency lending

- Other useful protections under CARES

Unemployment Insurance Expansion Under CARES

The major impact of CARES for the general workforce is the significant expansion of unemployment insurance (UI). UI benefits are set to increase $600 per week for up to four months, and federal funds will continue providing UI to those losing their jobs due to the COVID-19 pandemic for up to 13 weeks after state unemployment benefits have been exhausted.

The federal government is also creating incentives to encourage states to reduce their UI waiting periods so workers can maintain consistency of income following a layoff and looking to increase accessibility for the self-employed and others who have historically not qualified for UI.

Tax Credits Under CARES

From a dollars and cents perspective, CARES clarifies and defines the tax credits that legislators have been promising since the beginning of the coronavirus outbreak.

How to Understand Your Eligibility for CARES Tax Credits

Your eligibility (as an individual or business) for CARES tax credits depends on your 2019 tax return (or 2018 if you did not file last year). If you qualify for additional credits due to income/profit loss after your 2020 tax return, you will receive those as well. If you qualified during 2019 but do not based on 2020 filings, you still qualify.

CARES Tax Credits for Employers

CARES creates a variety of new employer tax benefits, including:

- A 50% refundable payroll tax credit on wages

paid up to $10,000 per employee is available for businesses posting a 50% or

worse return in gross receipts compared to the same quarter of last year

- For businesses with more than 100 employees, this credit applies to all workers on leave who are under your employ but not working

- For businesses with 100 or fewer employees, this credit applies to all employees

- A delay on employer-side Social Security tax payments until 1/1/2021

- A delay on aviation excise tax payments until 1/1/2021

- An exclusion of eligible student loan payments (up to $5,250 per employee) from taxable income calculations

- A suspension on the excise tax for alcohol used to make hand sanitizer for all of tax year 2020

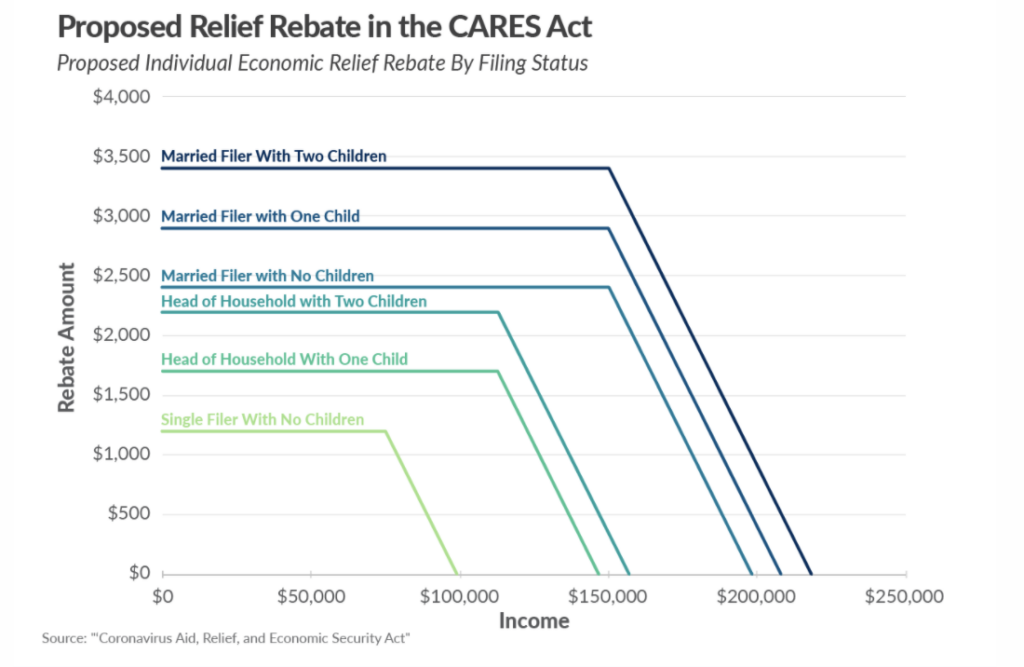

CARES Tax Credits for Individuals/Employees

CARES create a refundable tax credit (the “Recovery Rebate”) of $1,200 per individual or $2,400 per jointly filing couple plus an additional $500 credit for each child. Income limits/qualifications for those credits are as follows:

- Individual/Single taxpayers must have a taxable income of less than $75,000 to qualify for the full credit and less than $99,000 to receive any credit

- Heads of Household must have a taxable income of less than $112,500 to qualify

- Jointly filing couples must have a taxable income of less than $150,000 to qualify for the full credit and less than $198,000 to receive any credit

Access to Emergency Lending

In addition to providing tax credits for businesses affected by coronavirus, CARES also creates a $454 billion dollar emergency lending fund for businesses, states, and cities affected by the COVID-19 pandemic. The fund will be overseen by a Congressional Oversight Commission and a Special Inspector General.

The fund includes but is not limited to:

- $25 billion allocated for lending to airlines

- $17 billion allocated for lending to national security-critical organization

- $4 billion allocated for lending to cargo/shipping/supply chain firms

In order to qualify for these emergency loans, businesses:

- Must retain 90% of their March 24, 2020 employee count

- Must not engage in stock buybacks during the duration of the loan plus one year

Other CARES Considerations

Payroll Protection for Small & Medium-Sized Businesses

CARES creates a $350 billion Paycheck Protection Program fund for businesses with fewer than 500 employees struggling to make payroll or cover operational expenses between February 15 and June 30.

Technically, these funds are granted in the form of loans, but the loans will be forgiven as long as funds are used for payroll, rent, interest on mortgages. However, that loan forgiveness will be reduced proportionately if businesses shrink their workforce or reduce overall employee compensation 25% or more.

Eliminating Early Withdrawal Penalties for 401(k)s & IRAs

CARES waives the 10% early withdrawal penalty of 401(k)s, IRAs, and certain qualified trusts and annuities for individual taxpayers facing virus-related challenges. Withdrawn amounts will be taxed over the next three years, but individuals can also replenish the withdrawn funds during that same three-year period without affecting their cap.

This effectively unlocks long-term savings for a large number of Americans, making up for work reductions, layoffs, and other challenges facing individuals and families.

The Coronavirus Relief Fund

The CARES Act establishes a $150 billion Coronavirus Relief Fund for state and city government expenditures related to the coronavirus epidemic and resulting public health emergency. Funds will be divided based on population, with each state receiving at least $1.25 billion.

Takeaways

The CARES Act clarifies the federal government’s approach to economic protections for individuals and businesses during the COVID-19 outbreak, filling in many of the gaps in the language of the FFCRA and other recent guidance related to coronavirus. Specifically, the Act entails:

- $600/week unemployment insurance expansion

- Tax credits for lost productivity (for large businesses) and overall staffing impact (for small businesses)

- Tax credits for individuals based on their income and family size

- An emergency lending fund for businesses & municipalities

- Payroll protections for small businesses

- Eliminating retirement withdrawal penalties for individuals facing virus-based need